ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.

Proflex Wk 4-8 May — Chip Rally, Yield Reality, CPI Week

|

Proflex Market Update - Week 4 May - 8 May, 2026 Semiconductor Squeeze | Yield Reality | CTA Reversal | CPI Week "The rally is not fake. But when memory chips double in a month and the 30-year yield touches 5%, something has to give. The market is choosing not to ask which one."

— Proflex Panel

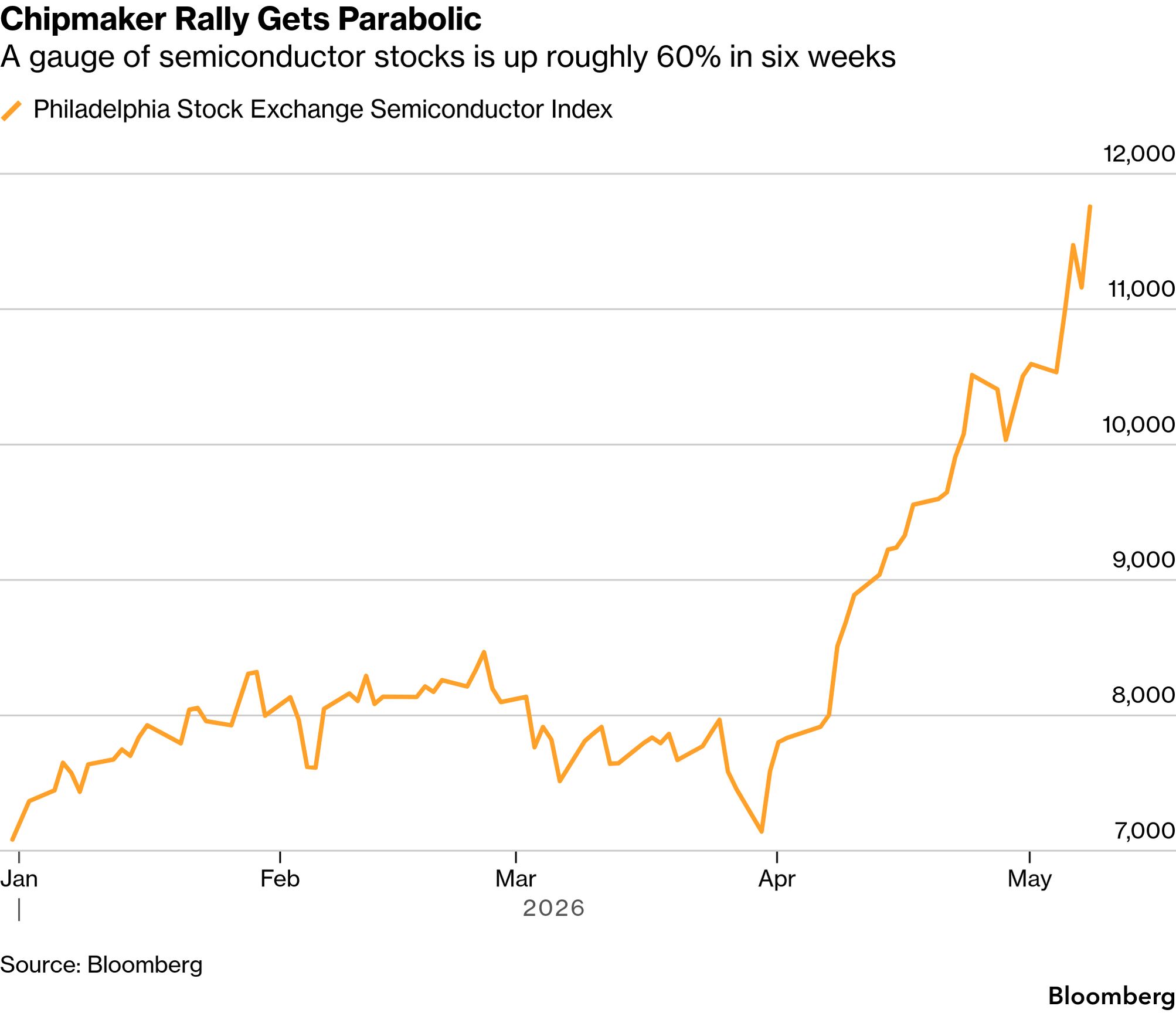

The S&P 500 pushed to 7,398 last week. A new high. By the headline number this is a bull market with no asterisk. Look one layer deeper and the asterisk is everywhere. QQQ has now been in overbought territory for 18 consecutive sessions: the longest stretch in a decade without a meaningful pullback. The breadth picture is the same one we flagged in Week 19 — only worse.

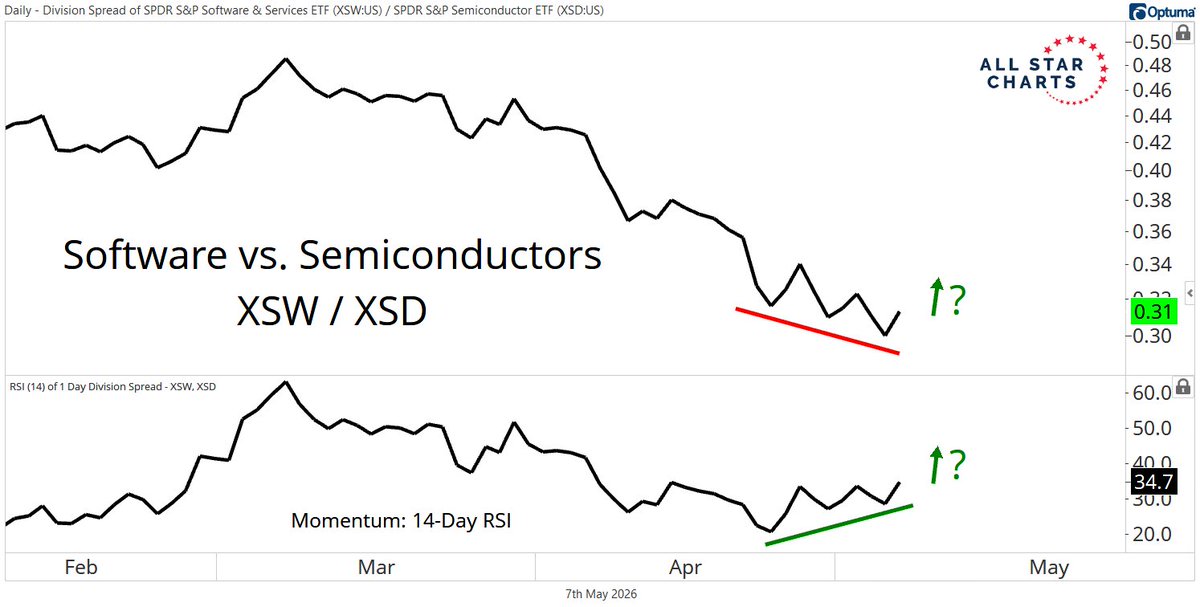

This is not a tech rally. It is a semiconductor chase, and the rest of the market is being dragged along by index weightings. Underneath it all, the macro backdrop has not changed.

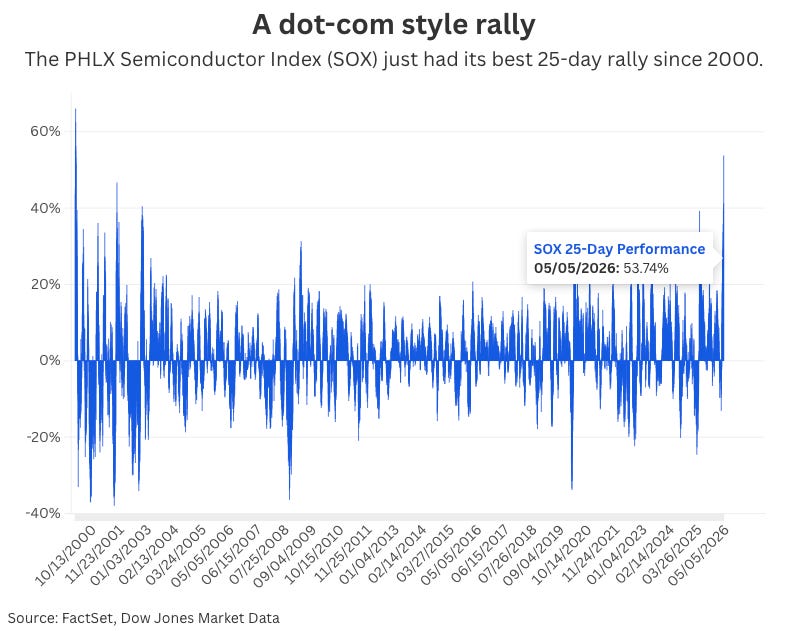

None of this is being priced into the semiconductor frenzy & we believe that gap will close. Insights from Proflex Macro CallThis week's session was shorter than usual but the message was direct. The central observation: this rally has no historical precedent. Not just in pace, but in structure.

Three specific warnings from the call:

Raman's Insight was simple: be very cautious chasing names that have already doubled. The drop from these levels, when it comes, will not be gentle. You can watch the complete recording here:

|

|

Memory prices have spiked as AI demand outpaced supply. These were real catalysts.

But the market is no longer trading the catalysts. The leaders of this actual AI cycle — Nvidia and Broadcom — have rather muted highs in this move.

Nvidia is near but not through its prior all time high. Broadcom is at same scale. The names gaining the most ground are the ones with the thinnest direct tie to AI revenue. That is a rotation signal, not a confirmation signal.

The deal integrity question adds another layer.

The Broadcom and OpenAI $18 billion custom chip arrangement requires Microsoft to commit to a substantial purchase before it closes.

Without that commitment, the deal does not proceed on current terms (The Information, May 8).

This mirrors the Oracle and OpenAI financing issues from earlier in the year, where banks refused to syndicate loans at scale due to single-borrower exposure limits.

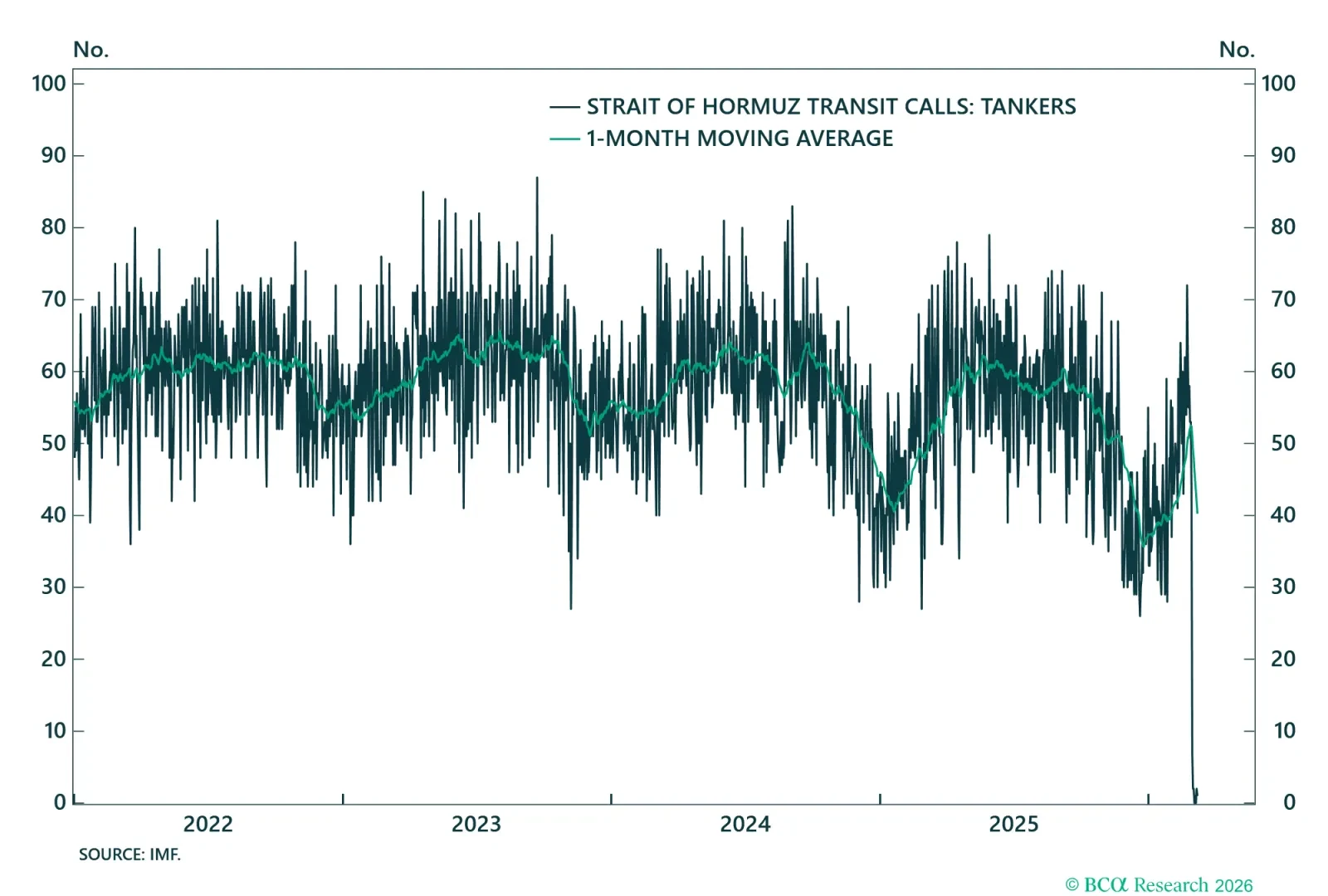

Oil, Yields, and the Macro That Isn't Going Away

The Strait of Hormuz has not reopened. Monthly vessel traffic has collapsed from a pre-war baseline of roughly 3,000 ships to 191 in April — a 94% reduction.

Iran seized another oil tanker on May 8 and formally established the Persian Gulf Strait Authority the same week. This is not moving toward resolution.

|

Brent is at $103 . March PPI already came in at +4.0% year over year, with energy alone up 8.5% in a single month.

April CPI — the first full print to capture the oil surge at scale — releases Tuesday. Consensus is at 3.7 to 3.8% headline.

CME FedWatch is pricing zero rate cuts in 2026, with the first cut not expected until the second half of 2027.

The market has been running a split screen for weeks: semiconductor momentum on one side, energy disruption and rate pressure on the other.

CTA Reversal: The Structural Bid Has Shifted

In Week 18, we noted that CTAs had reached the 100th percentile of net long positioning: the full extent of their buying capacity. That positioning was one of the key mechanical supports keeping the market from correcting as the macro deteriorated.

That support has now changed direction. BofA's latest estimates (data through May 8) show the following:

- Flat market: CTAs are buyers of just +$0.4 billion — down from +$33 billion the week before

- Up market: CTAs become sellers of $21 billion

- Down market: CTAs become sellers of $77 billion

The cushion that absorbed every dip since March is gone.

CTAs have moved from structural buyers to sellers on any down tape.

Combined with a VIX at 17, the current market structure has a specific profile: very little insurance in the system, and the largest mechanical seller now activated on any meaningful decline.

This echoes the options scaffolding dynamic we flagged in Week 11 before the March expiry. The protection mechanism flips, and the market is suddenly trading without the floor it had grown accustomed to.

CPI, Treasury Demand, and a Fed Chair Transition

This is one of the heavier data weeks of the year. The market is being asked to hold all time highs through a compressed sequence of catalysts:

- Tuesday, May 12 — April CPI. Consensus: 3.7 to 3.8% headline, 2.7 to 2.9% core

- Tuesday, May 12 — $42 billion 10-year Treasury auction

- Wednesday, May 13 — April PPI. March came in at +4.0% year over year

- Wednesday, May 13 — $25 billion 30-year Treasury auction

- Thursday, May 14 — April Retail Sales

- Friday, May 15 — Jerome Powell's term as Fed Chair ends

Kevin Warsh is expected to be confirmed by the Senate this week. The Banking Committee passed his nomination 13 to 11 — the first fully partisan Fed chair committee vote in history.

Senator Fetterman is expected to cross the aisle, giving Warsh the votes he needs before Powell's term expires Friday.

The 30-year auction Wednesday carries the most weight. With the 30-year yield still close to its cycle high at 4.94%, weak overseas demand — particularly from Japan, where yen dynamics have changed the incentive structure for US duration — could push long rates higher at exactly the moment markets are absorbing an inflation print and a leadership change at the Fed.

|

🧭 Proflex Playbook – Discipline in an Stretched Rally

With corporate earnings, War in Intermediation & Insitutional Reversal, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

| Proflex All-Access Subscription (Yearly) |

| Proflex All-Access Subscription (Monthly) |

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures

Proflex Institutional Research Series

ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.