ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.

Proflex Wk 25-29 May — Blue Sky Melt Up, Software Breakout, Bitcoin's Cycle

|

Proflex Market Update - Week May 25 - May 29, 2026 Blue Sky Melt Up | Software's Comeback | Bitcoin's 4Y Cycle | The Euphoria Signals “The market has decided that war, high yields, and hot inflation no longer matter. That conviction is exactly what makes it fragile."

— Proflex Panel

The rally has gone vertical, and it has stopped listening to bad news.

This is a blue sky breakout.

When volatility is this cheap, almost no protection is being bought, and the air pockets underneath the market get deeper. The question this week is not whether the rally can keep running. It clearly can. The question is what happens to a market priced for perfection the moment a single assumption (oil, the Fed, AI ROI) cracks. Insights from Macro CallThis week's call was a study in discipline over momentum. Raman walked through why this is one of the most dangerous markets to invest in fundamentally, even as it keeps making new highs. A few ideas stood out:

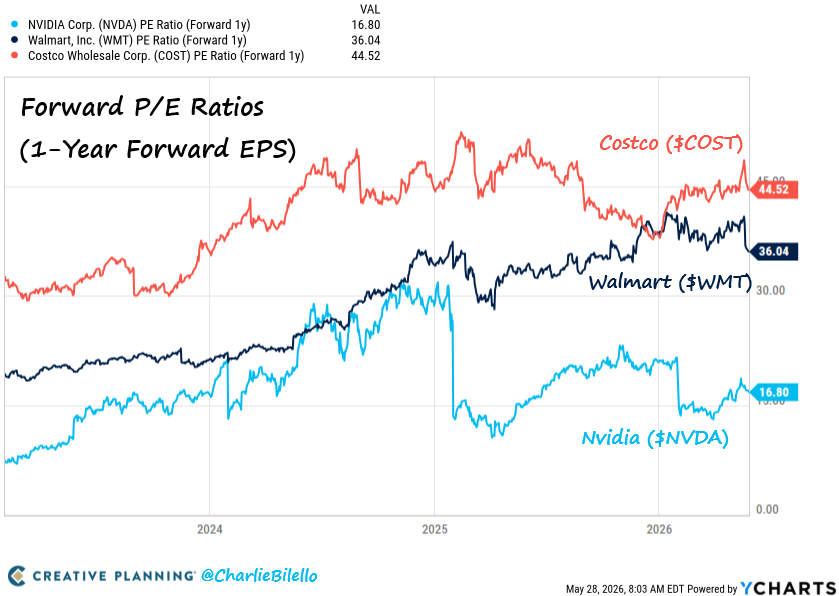

You can watch the complete recording here: Key Drivers This WeekThe Blue Sky Melt Up: Narrow, Parabolic, Priced for Perfection We have broken out of the long-term trend and into a zone with no resistance overhead. That is the good news. The valuation split is where it gets uncomfortable. NVIDIA, the genuine cash machine that printed close to 90% earnings growth, trades on a sober ~16x forward and actually corrected on its results.

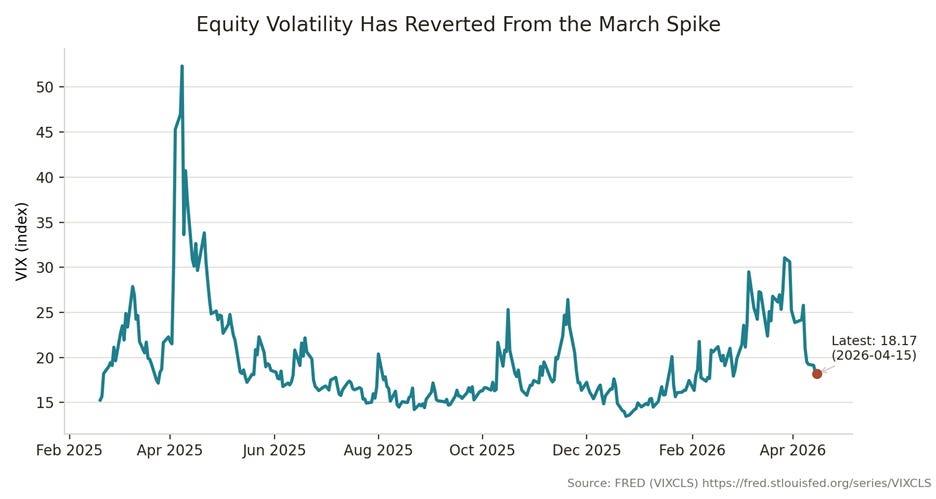

Proflex View: This is not a market to fight, but it is a market to respect. With the VIX near 16, the protection is gone and the air pockets are deep. We would rather miss the last leg of a parabola than be the one holding it when month-end gamma and a single macro headline collide. Discipline over direction. Software's Quiet Comeback For six months the story was simple: AI eats software, and the IGV software index put in its weakest start since 2008.

The reason is the AI ROI reckoning.

Proflex Takeaway: The software names were beaten down on a threat (AI replacement) that has not shown up in their earnings. They are no longer pure software anyway; many are becoming infrastructure and data-center plays. We do not know if the rotation holds in a market this irrational, but the setup (oversold, profitable, mispriced for death) has clear merit.

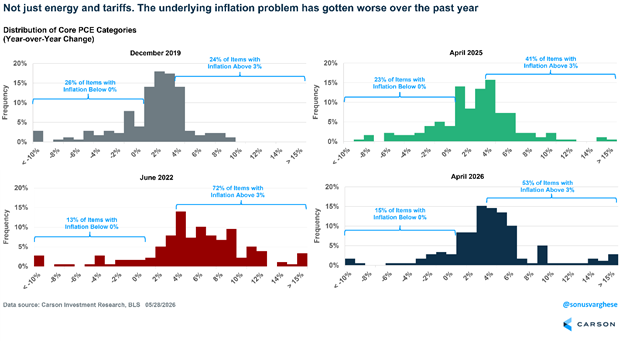

Oil, Yields, and the Rate-Cut Vacuum Oil is finally cooling off the war premium. Brent is back near $96 and WTI near $93, down from the $120+ Dubai-crude spike in March.

That hot inflation is why the rate-cut hope has evaporated. Markets now price essentially zero cuts through year-end (a ~51% probability of no cut at all), against the two cuts expected earlier in the year.

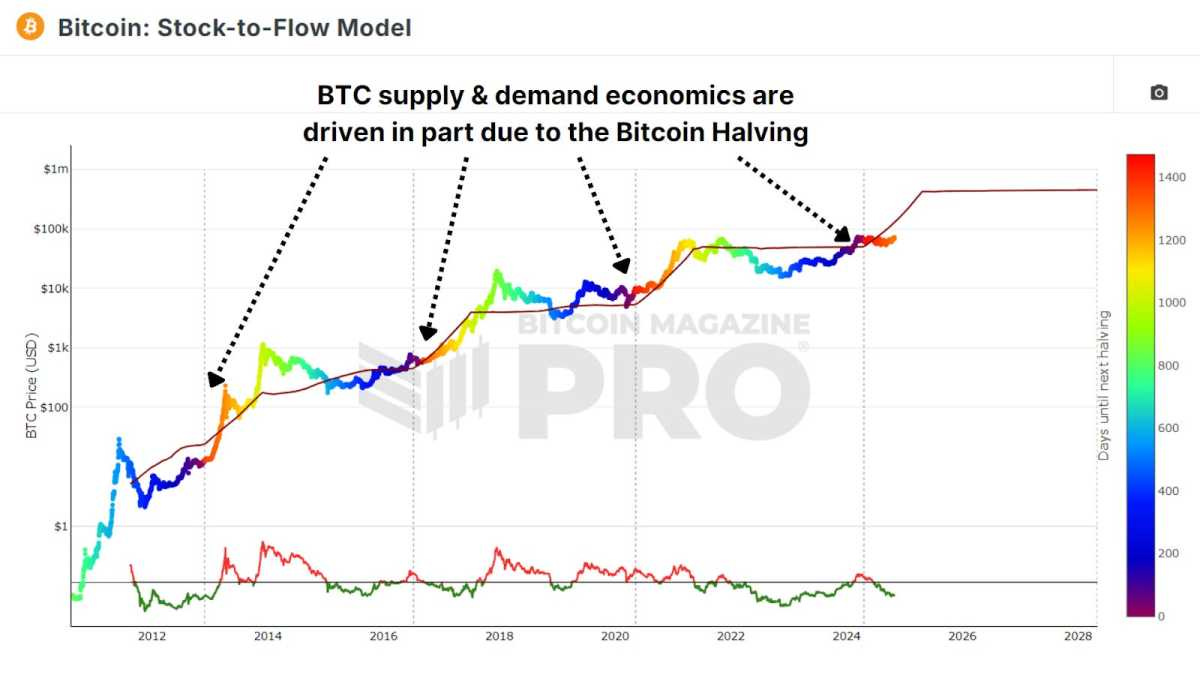

Proflex View: Oil is the master variable again. A clean break below $80 would do more for risk assets and gold than any Fed speech. The risk is the two-sided trap: an actual resolution could be a "sell the news" event after a run this large, or it could fuel another leg higher. We position for both, not for one. Bitcoin's Four-Year Cycle and Gold's Euphoric Reset Bitcoin is the clearest casualty of the AI euphoria. It has been rejected at its 200-day on a weekly basis and slid to roughly $72,000, off about 43% from the ~$126,000 October peak, with thin support and a path that could test $68,000 and the long-term trend line. The supply side is heavy.

Miners are adding to the pressure, transitioning data centers from mining to AI and funding the pivot: IREN's $9.7B Microsoft deal, Core Scientific's $10B CoreWeave deal, Hut 8's $7B Fluidstack lease, with some miners on track to earn 70% of revenue from AI hosting by year-end. Gold tells the other half of the story.

We called the top after its euphoric run back in January and February, and it has corrected hard since (a drawdown near 27%), even though the Iran war was fundamentally bullish for it.

Proflex Watch: Both assets remain relevant for a fractured monetary world: gold for the sanctioned, approved channels, Bitcoin for the unsanctioned ones (recall Iran reaching for crypto to settle around blockades). Bitcoin needs time and the halving; gold needs the yields to ease. Neither thesis is broken. Both are simply out of favor while the AI mania owns the attention. 🔍 What We’re Watching

🧭 Proflex Playbook – Discipline in an Stretched Rally

Proflex All-Access: Your Market Compass

Explore the financial markets with Proflex All-Access, your comprehensive resource for deeper market understanding and active participation. This premium service offers subscribers exclusive insights and actionable investment advice, giving you a significant edge in various market conditions.

Proflex All-Access provides detailed analyses and recommendations to optimize your investment strategy. Our specialized newsletters include:

• Growth Gazette (Contains Crypto Pulse) : Aimed at achieving above-market returns for aggressive portfolio growth.

• Income Insider: Focused on conservative strategies and income generation for yield-seeking investors.

ProFlex® by Blockstart Research

Legal Disclosures ProFlex® by Blockstart Research, the premium newsletter product series, provides informational and educational content only and does not offer personalized investment advice or establish a fiduciary relationship. While we rely on reliable sources and research, the information is not tailored to individual financial situations. Readers are urged to consult qualified financial professionals before making investment decisions. We do not guarantee the accuracy, completeness, or timeliness of the information and are not responsible for any investment decisions based on this newsletter. Investing carries risks, and past performance doesn't predict future results. By accessing this newsletter, you acknowledge that we are not liable for actions or decisions resulting from its content. Please conduct due diligence and seek professional advice as needed.

|

Proflex Institutional Research Series

ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.