ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.

Proflex Wk 18-22 May — NVDA Earnings, SPX 7,500, Iran Deal Watch

|

Proflex Market Update - Week May 18 - May 22, 2026 NVDA Blowout | SPX 7,500 | Iran Deal Watch | Warsh Era Begins “Eight consecutive weeks of S&P gains. NVIDIA guiding to $91 billion. Brent down $20+ from its April peak & a new Fed chair sworn in with zero rate cuts priced through year end. This market is repricing everything at once and the easy part is behind us.”

— Proflex Panel

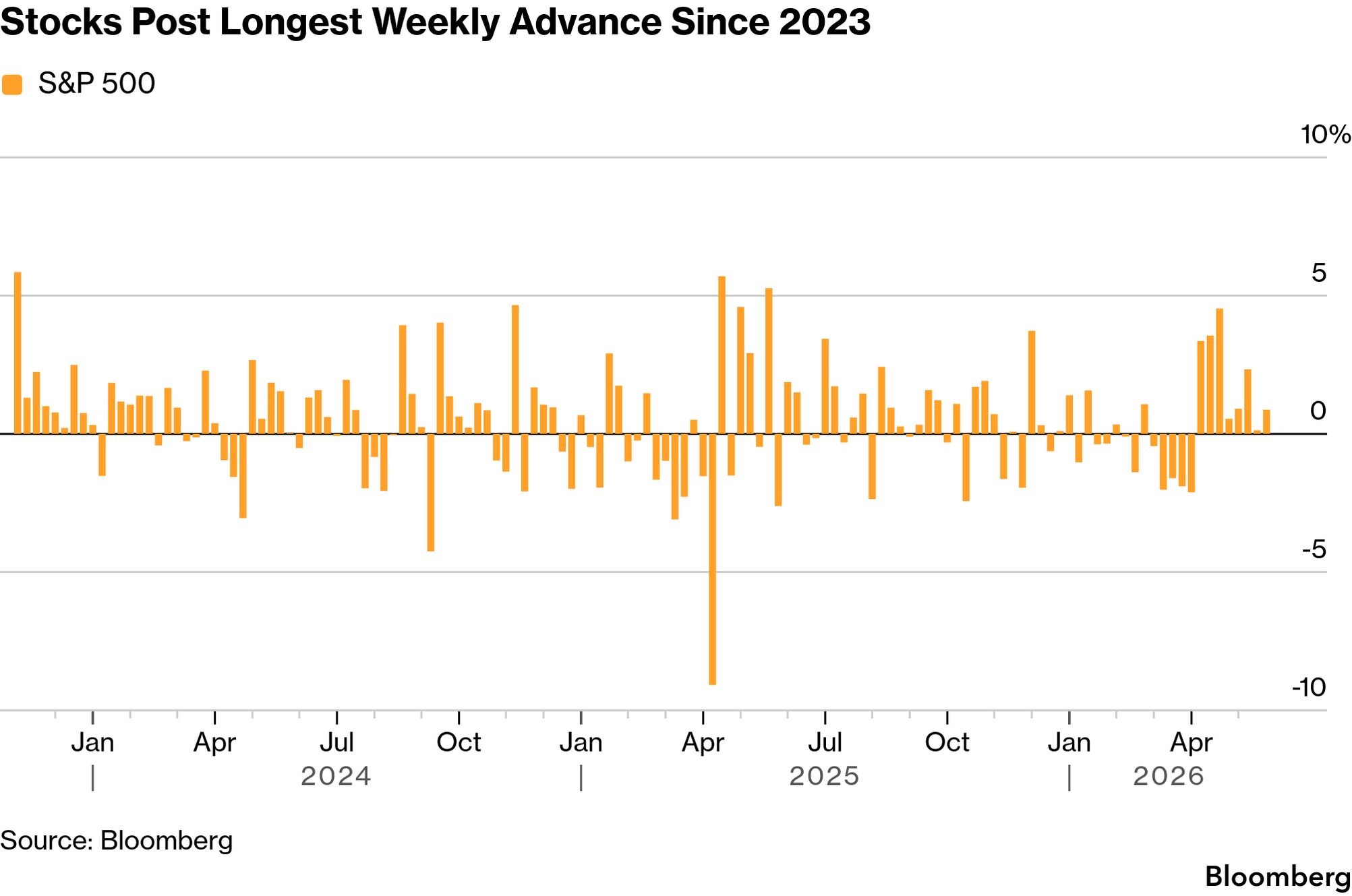

The S&P 500 crossed 7,500 last week for the first time in history. Eight consecutive weekly gains which is the longest streak since December 2023 with VIX sitting at 16-17 and the index up 5.22% over the past month.

The first engine is Iran deal optimism.

Then on Friday, Kevin Warsh was sworn in as Federal Reserve Chair confirmed by the Senate 54-45, the closest vote in modern Fed history — and immediately declared he would lead a “reform oriented Federal Reserve.”

The next leg of this rally gets earned differently than the last eight weeks. Here is what actually matters.

|

|

Huang on the call: "Nvidia is the only platform that runs every frontier AI model" — naming Anthropic, OpenAI, SpaceX AI, Meta, and Google Gemini in a single breath.

The next-generation Vera Rubin platform targets a $200 billion TAM in agentic AI alone.

The ecosystem is widening.

- Broadcom reported AI chip revenue of $8.4 billion (+106% YoY) for Q1, guiding to $10.7 billion in Q2.

- AMD's data center revenue hit $5.8 billion (+57% YoY). The SOX semiconductor index is up 74.5% YTD.

We've said this before: This is no longer a single-stock story rather it's a capital cycle event that is drawing in every infrastructure layer from chip design to power to cooling.

One overhang worth naming:

Huang acknowledged NVIDIA has "largely conceded China's AI chip market to Huawei" due to US export restrictions.

That's not a near-term revenue surprise: China was already ring-fenced from high-end GPU exports but it's a long-term market share reality the bulls need to hold alongside the supercycle thesis.

As we noted in Wk 20 when QQQ RSI sat in an 18-consecutive-session overbought window: the thesis was never "the trade is over" rather it was "the easy phase is over."

Post this print, that distinction is sharper. The secular AI case is as strong as it has ever been. Entry discipline is what matters now, not conviction.

The S&P at 7,500: Eight Weeks, Three Engines

We covered the three engines in the opening — AI earnings, Iran deal relief, and CTA positioning — but the risk picture sitting underneath the index is worth looking at directly.

The 10-year yield is holding at 4.56%, persistently elevated. Month end rebalancing supply arrives this week on top of Memorial Day liquidity conditions, which historically amplify moves in both directions on thin volume.

|

The advance/decline line shows a rally that is narrower than the index headline suggests — the biggest names are doing the heavy lifting while the median stock remains well below its 52 week high.

The fundamental case is intact. Blended earnings growth tracking +23% for 2026 is real. The AI capex cycle is confirmed.

And if the Hormuz MOU closes, the oil relief alone could unlock the rate cut math the market has been waiting for since January. But the CTA bid that powered the April recovery is spent. The next incremental buyer needs a reason, not just momentum.

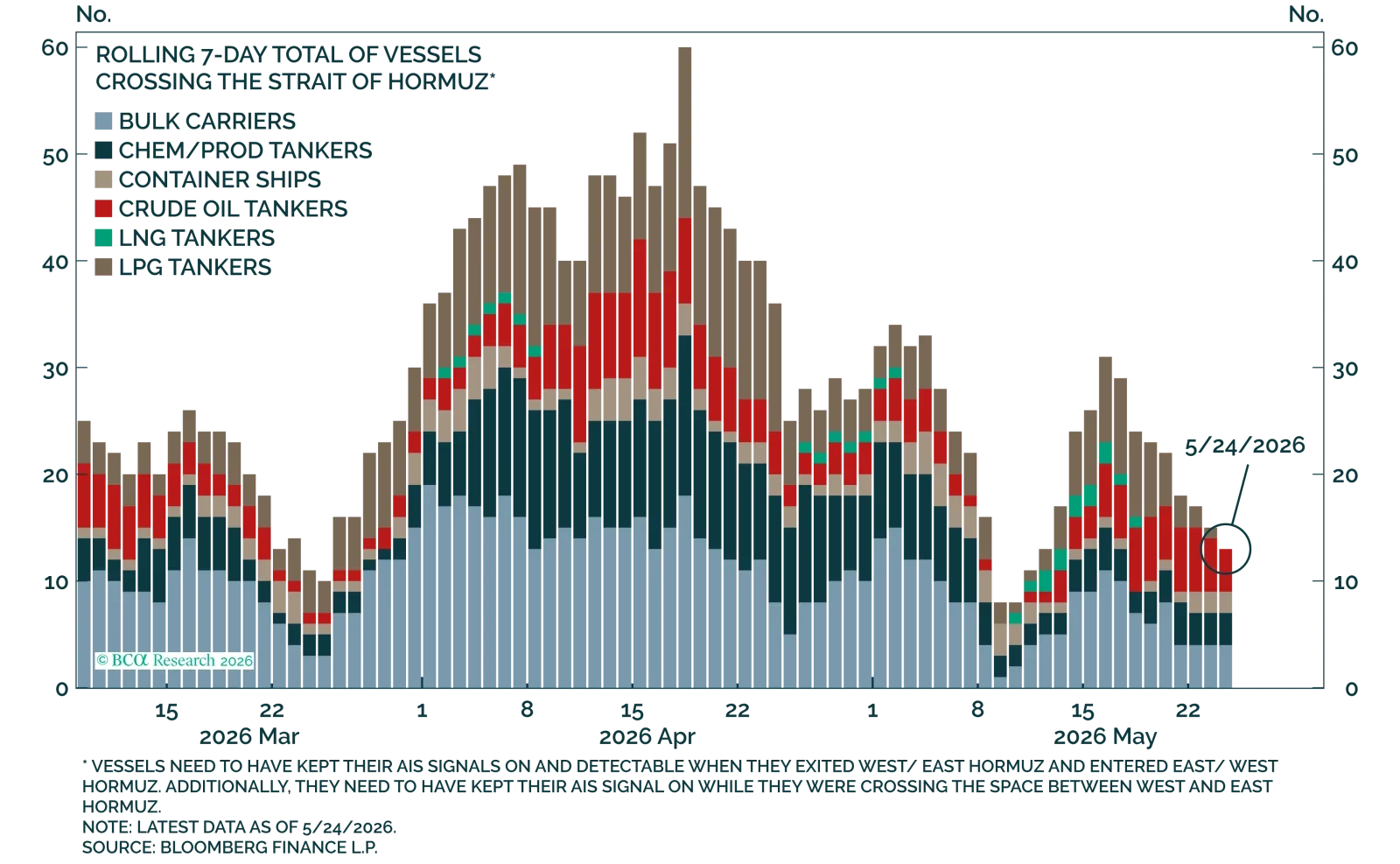

Iran: Deal or Delay — The Strait at 2%

The Strait of Hormuz remains effectively closed. Two vessels transited as of May 17 — 2% of normal volume.

More than 1,550 commercial ships are stranded with 22,500 mariners aboard.

|

Every major insurer has cancelled coverage. Maersk, MSC, CMA CGM, and Hapag-Lloyd remain suspended. The Strait has been the single most important variable in the global inflation picture for three months. It has not moved.

And yet the market is running on deal optimism — and this time it actually has a foundation.

Trump declared on May 24 that the MOU is “largely negotiated,” with talks mediated through Pakistan covering: a temporary moratorium on uranium enrichment, sanctions relief sequencing, and a phased maritime reopening.

The UAE, Saudi Arabia, and Qatar jointly urged Trump on May 22 not to restart full hostilities, a significant signal from three Gulf states that have been divided on this conflict throughout. April CPI landed at 3.8% YoY, the highest since May 2023, driven by a 17.9% YoY surge in energy.

The economic incentive to resolve this is overwhelming on both sides.

The complication: CENTCOM conducted new strikes on Iranian vessels and missile sites on May 25 — the same day Trump called it a work in progress.

Three US Carrier Strike Groups are simultaneously deployed in the region for the first time in decades. The ceasefire is technically in effect and actively violated at the same time.

Two scenarios remain:

- Resolution: MOU closes in the next two to three weeks, Hormuz reopens on a phased timeline, Brent falls toward the $75 to $85 range. CPI path toward 2.5% by Q4 reopens the rate cut conversation for Warsh at the September FOMC.

- Fracture: Talks collapse on the enrichment red line, strikes escalate, Brent reasserts toward $110 to $120. Zero cuts become one hike. Stagflation goes from Wall Street debate to Main Street reality.

The Warsh Era: What Changes at the Fed

Kevin Warsh was sworn in as Federal Reserve Chair last Friday, May 22 — confirmed by the Senate 54-45, the closest vote in modern Fed history, officiated by Justice Clarence Thomas at the White House.

His first words in the role: “I will lead a reform oriented Federal Reserve.”

The bond market reacted immediately. The 30-year Treasury yield touched 5% for the first time since 2007.

Traders now price zero Fed rate cuts in 2026, down from three cuts expected just months ago.

A futures outlier now prices a 61% probability that rates are higher by year end than today.

What changes under Warsh — and this matters for how you read every Fed signal going forward:

- Press conferences after every meeting: likely gone. Warsh has criticized Powell’s approach as excessive communication. Markets will have less real time guidance.

- The dot plot: under review. Warsh opposes publishing rate projections, calling it “false precision.” Its removal would create a significant forward guidance void the bond market will need to reprice.

- Balance sheet: targeted for reduction. He has called it “particularly unhelpful.” Not a fast process — but the direction is clear.

- Inflation target: softer framing. Warsh’s stated goal is “a price environment where no one’s talking about it” rather than a hard 2% ceiling. He cited AI driven productivity as a “significant disinflationary force” — an unusual anchor for an opening statement from a new Fed chair.

His first FOMC press conference is June 17. The FOMC blackout period begins May 29 — no Fed speak this week. That June 17 presser is the first real read on whether his reform instincts translate into dovish flexibility or hawkish resolve.

The key question for June 17: does his AI productivity thesis give him cover to ease earlier than the market expects, or does 3.8% inflation lock him into a hold? Until that press conference, the bond market is writing his chapter. We watch the 10-year at 4.56% and the 30-year’s flirtation with 5% as the leading indicator.

🔍 What We’re Watching This Week

- PCE — Thursday May 28. The Fed’s preferred inflation gauge. April core PCE after a 3.8% CPI print is the critical input for Warsh’s June 17 framing. A soft print cracks the rate cut door open. An upside surprise deepens the zero cuts narrative.

- Tanker transit data. Not diplomatic statements. Actual vessels moving through Hormuz. Two per day is still a closed strait regardless of what any press conference says.

- June 17 FOMC. Warsh’s first press conference. Dot plot fate, balance sheet timeline, and his read on AI as a disinflationary force will each move markets independently.

- S&P breadth this week. Memorial Day liquidity conditions historically amplify moves in both directions. A narrow leadership push to new all time highs on thin volume needs confirmation the following week before adding exposure.

🧭 Proflex Playbook – Discipline in an Stretched Rally

With corporate earnings, War in Intermediation & Insitutional Reversal, we see the market to absorb signification shocks. But the speed of this move demands respect, not complacency.

Our conviction stays anchored in the data:

- Focus on Structural Growth: Continue to overweight the secular AI theme, recognizing its multi-year runway.

- Anticipate Shallow Corrections: Use dips as accumulation opportunities, not reasons for fear, understanding that "none of the corrections stick."

- Diversify Thoughtfully: Recognize the "decorrelation" across asset classes; consider gold, silver and Bitcoin for portfolio resilience.

- Develop Mental Models: Prioritize long-term planning (6-12 months out) over short-term news, aiming for consistent, incremental gains.

If you're an All-Access or Managed Portfolio subscriber, our positioning has already shifted ahead of this moment—scaling up asymmetric hard asset plays while hedging for earnings volatility and geopolitical tail risks.

| Proflex All-Access Subscription (Yearly) |

| Proflex All-Access Subscription (Monthly) |

Until next week,

— The Proflex Team

Trusted Macro Insights. Calm Investing. Tactical Trades.

Legal Disclosures

Proflex Institutional Research Series

ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.