ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.

Proflex Wk 1-5 Jun — Worst Day Since October, Memory Crash, IPO Liquidity Drain

|

Proflex Market Update - Week Jun 1 - Jun 5, 2026 The Rally Finally Stops | Memory Crash | The Gamma Trap | Bitcoin's Last Support “The most fragile market is the one that has stopped believing it can fall. This week, it remembered."

— Proflex Panel

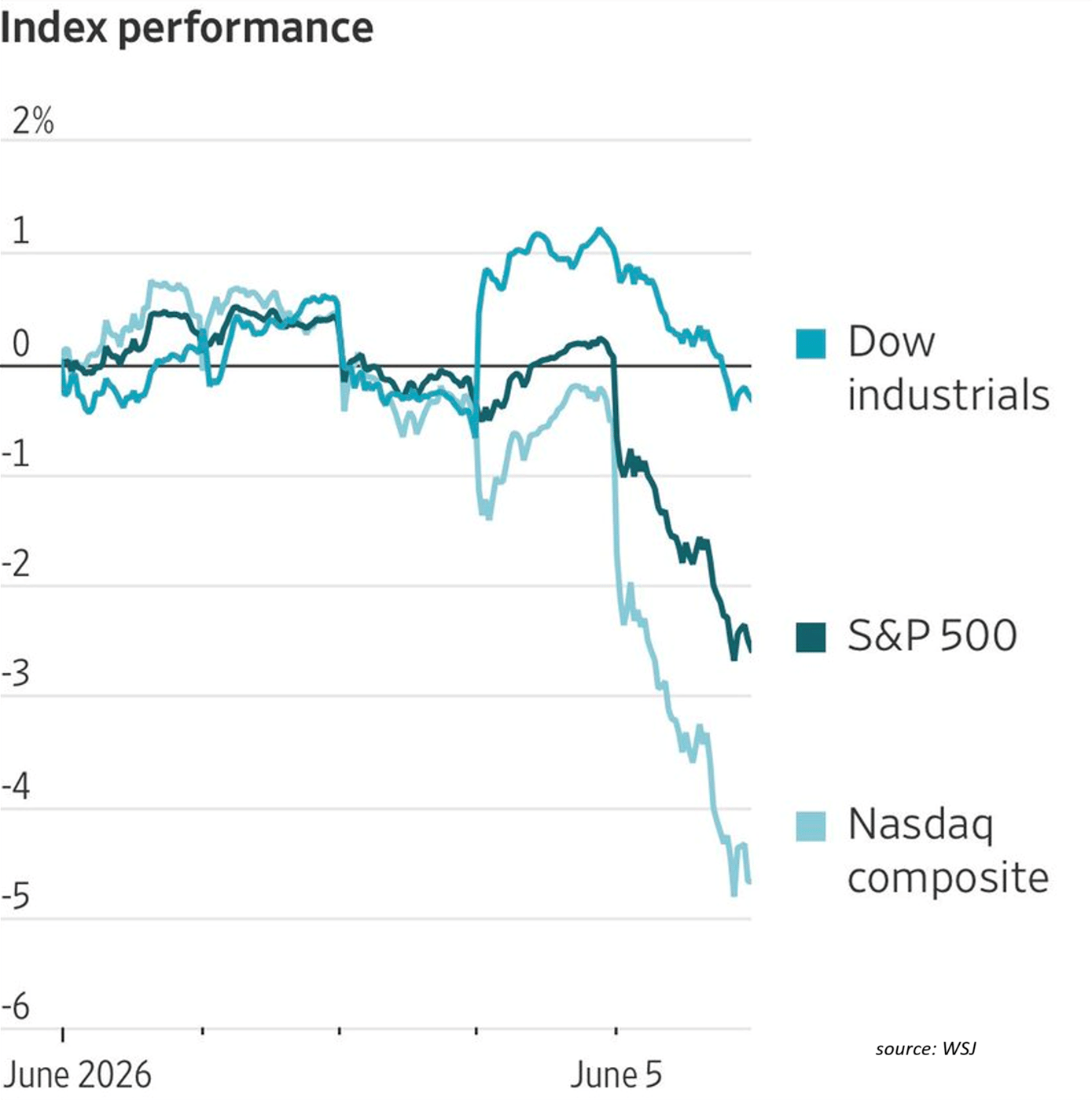

The rally stopped after 9 consecutive positive weeks. Friday delivered the worst session for the S&P 500 since October.

Two weeks ago, in the Blue Sky Melt Up edition, we wrote that the floor was thin, that the VIX near record lows meant almost no protection was being bought, and that drops turn violent when the air pockets are this deep. So the question is the one that always follows a day like this: is the rally over, or did something simply snap that can snap back just as fast? Insights from Macro CallThis week's call was about separating a structural break from a mechanical one. A few ideas Raman walked through directly:

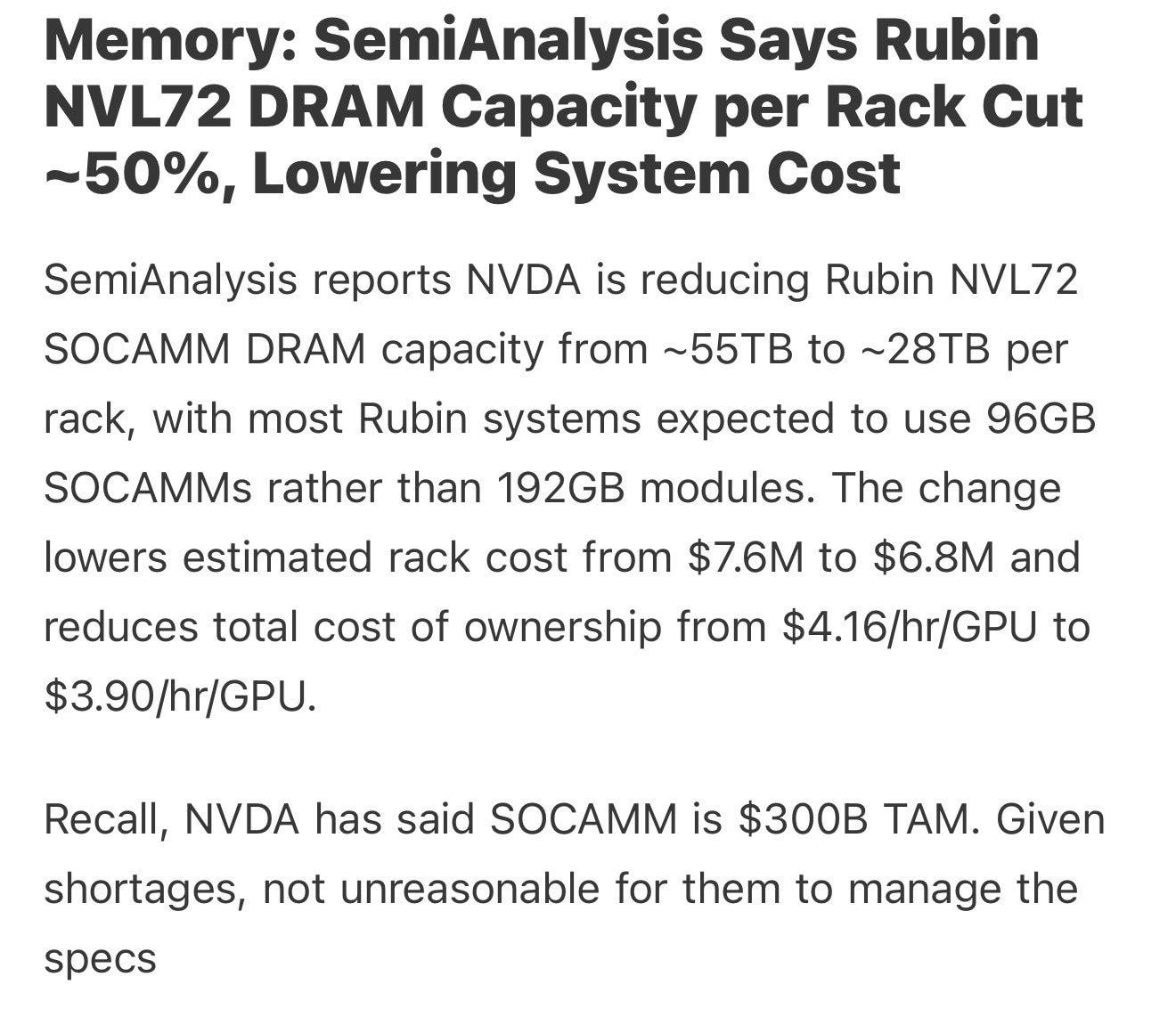

You can watch the complete recording here: Key Drivers This WeekMemory Mania and the Korea Overnight The break started where the rally was most stretched. Then the story turned overnight.

Korea opened in freefall, the KOSPI tripped its circuit breaker with an 8% plunge, and the selling rolled west into the US session. SMH fell close to 10%.

The cruel part: the ETF machinery dragged down NVIDIA and Broadcom too, the names that actually delivered, simply because they sit in the same baskets.

Proflex View: This is mispricing and not a verdict. It cannot be true that memory stays in permanent shortage while NVIDIA, the best performance per watt silicon on the planet, loses demand. When NVIDIA trades near 24x forward and second tier story chips ride triple digit multiples, the correction is doing the market's homework for it. Expect the recycling to continue, and watch for the rotation into names that never participated.

The Gamma Trap: Why There Was No Bid The reason Friday felt different is structural.

We flagged this exact mechanic back in March around the quarterly expiry: when volatility is cheap, almost no insurance gets written, and the protection that normally cushions a drop vanishes right when you need it.

Proflex Takeaway: A mechanical break can reverse as fast as it arrived. A weekend to digest the news, a flat tape, and a few buyers returning can repair a lot of this by early next week. But the bigger quarterly expiry lands June 18, and the fragility does not clear until then. Respect the air pockets.

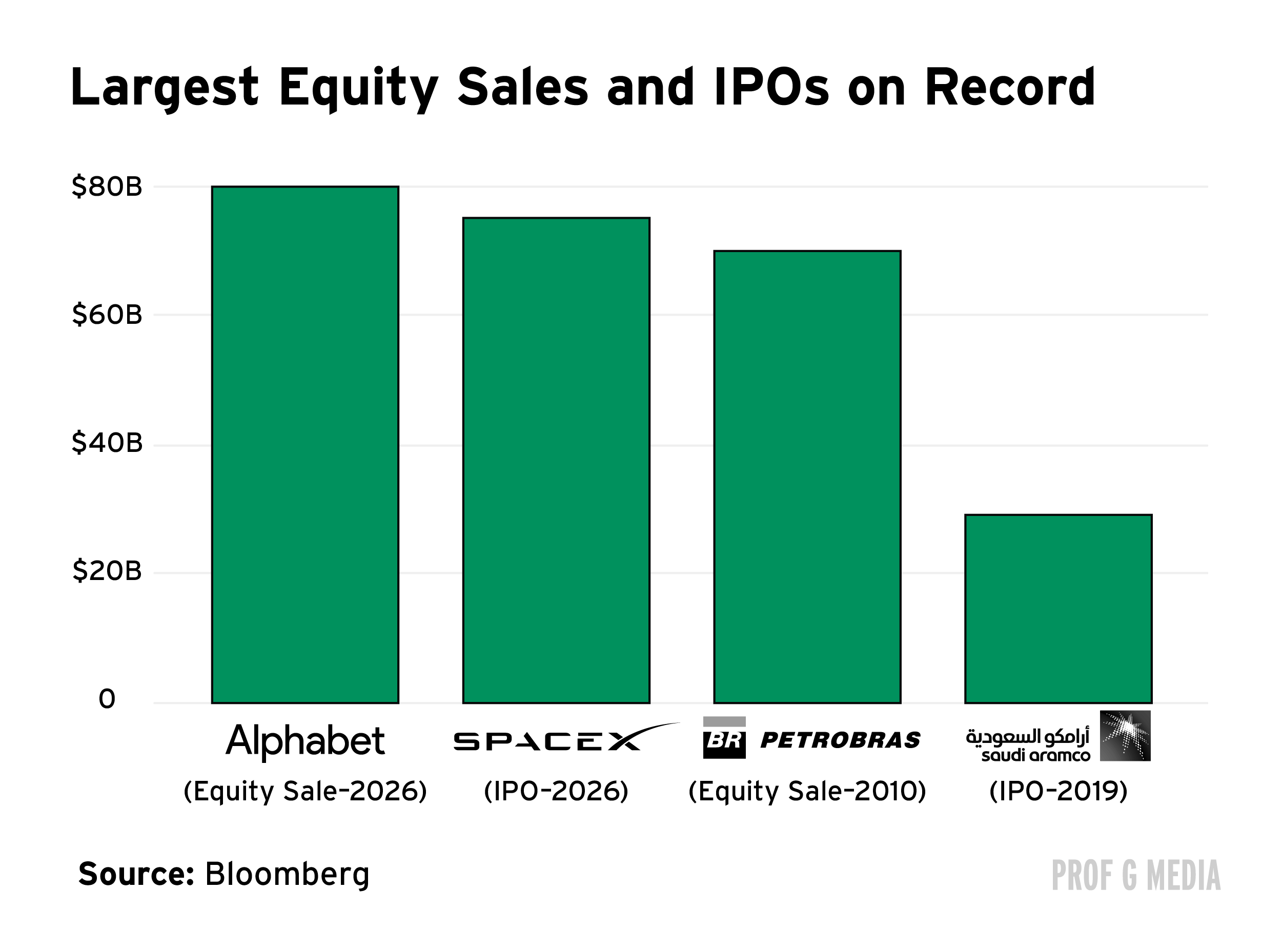

The Liquidity Drain: Who Funds the Next Half Trillion This is the theme with real legs. The market has spent two years assuming AI capex would be paid out of free cash flow. That assumption is breaking. With oil and yields keeping debt expensive and free cash flow compressing under capex, the CFO maths has flipped: when your equity trades at AI era multiples, issuing stock is the cheaper way to raise money. Google moved first.

The pipeline behind it is heavy:

Stack it up and the market may need to absorb several hundred billion in fresh supply in quick succession.

A market can levitate on thin trading volume, but it cannot fund half a trillion of new issuance without selling existing stock to do it. To be fair, this is not unanimous.

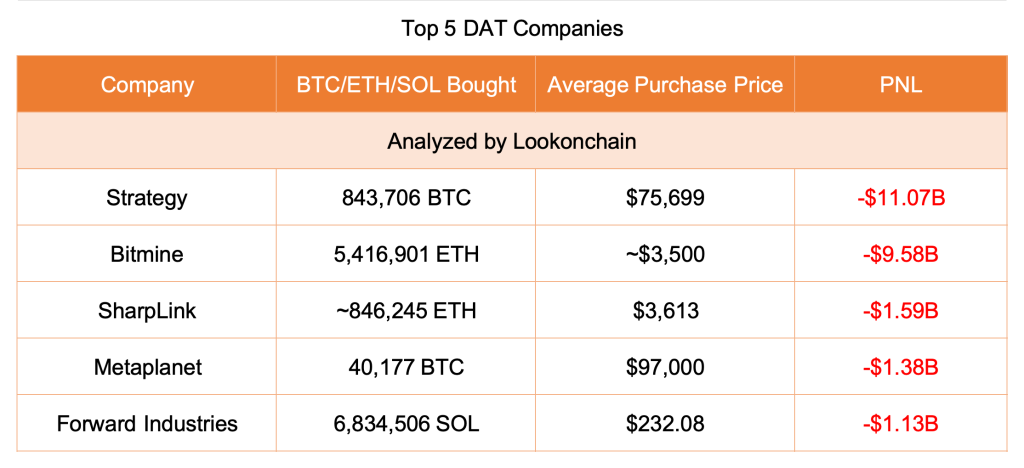

Proflex View: Nobody is saying these raises are irrational. The capabilities are real and the IPOs are genuinely exciting. The point is sequencing. A market priced for perfection does not need a recession to wobble, it just needs to wonder where the next buyer's cash comes from. If SpaceX lists poorly, every IPO behind it gets repriced, and that is the variable to watch. Bitcoin Tests Its Last Line Bitcoin has become the cleanest macro proxy we track, and the macro has not been kind. Two forces are compounding it.

Proflex Watch: Below the trendline sits a deep support shelf in the $50,000 to $60,000 zone, but most investors who arrived in the ETF era have never seen those levels and are now underwater, which feeds the outflows. Zoom out: this is the four year cycle doing what it always does. The 2022 low printed in November, and history says a cycle bottom has a real chance of forming somewhere in 2026. Gold Holds, Oil Surprises, and the Macro Quietly Improves Three quieter signals worth holding onto:

Proflex Watch: High inflation, no cuts, but rate hikes are far less likely than Friday's bond move implies. The macro is not the problem this week. Positioning is. The value is building in the names this rally left behind, and the rotation will come once the forced selling clears. Stay cautious into the June 18 expiry, then let the tape tell you. 🔍 What We’re Watching

🧭 Proflex Playbook – Discipline in an Stretched Rally

Proflex All-Access: Your Market Compass

Explore the financial markets with Proflex All-Access, your comprehensive resource for deeper market understanding and active participation. This premium service offers subscribers exclusive insights and actionable investment advice, giving you a significant edge in various market conditions.

Proflex All-Access provides detailed analyses and recommendations to optimize your investment strategy. Our specialized newsletters include:

• Growth Gazette (Contains Crypto Pulse) : Aimed at achieving above-market returns for aggressive portfolio growth.

• Income Insider: Focused on conservative strategies and income generation for yield-seeking investors.

ProFlex® by Blockstart Research

Legal Disclosures ProFlex® by Blockstart Research, the premium newsletter product series, provides informational and educational content only and does not offer personalized investment advice or establish a fiduciary relationship. While we rely on reliable sources and research, the information is not tailored to individual financial situations. Readers are urged to consult qualified financial professionals before making investment decisions. We do not guarantee the accuracy, completeness, or timeliness of the information and are not responsible for any investment decisions based on this newsletter. Investing carries risks, and past performance doesn't predict future results. By accessing this newsletter, you acknowledge that we are not liable for actions or decisions resulting from its content. Please conduct due diligence and seek professional advice as needed.

|

Proflex Institutional Research Series

ProFlex® is designed to optimize your time, ignite your investment IQ, and maximize your financial potential.